In depth analysis of the decoration industry chain and the rise of precast decoration

The traditional architectural decoration ushers in innovation.

According to the latest statistical caliber, in the subdivision fields of China’s decoration industry: the public decoration field includes the decoration of public places, the decoration of government owned buildings, the decoration of hardbound buildings and the decoration of affordable housing; The field of home decoration includes home room decoration; Curtain wall field includes curtain wall decoration of commercial buildings, public buildings and high-end residential buildings.

At this time, there were construction individuals and teams with relevant skills in this field.

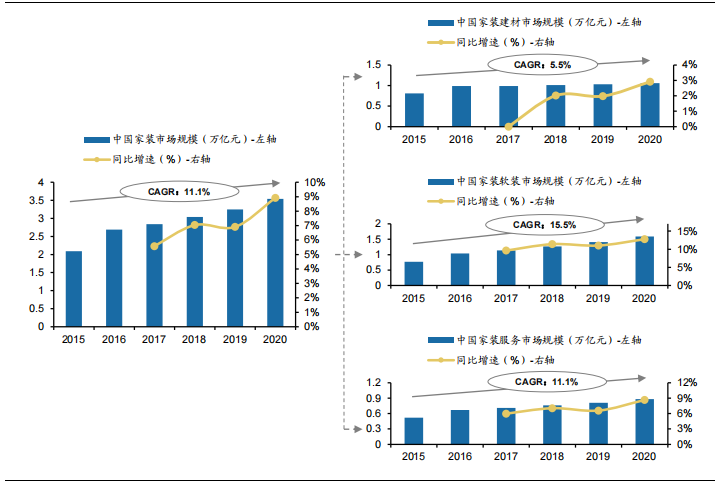

Figure 4: data source of the total output value of China’s public decoration industry: EU billion think tank, Deloitte decoration, GF Securities Development Research Center ❷ the growth rate of the home decoration market has increased, the speed of the soft decoration market has increased significantly, and the growth of the home decoration building materials market is relatively stable.

Benefiting from the promotion of urbanization, the upgrading of consumption structure and the gradual release of secondary decoration demand, the market space of the decoration industry will continue to grow.

It is expected that the total output value will reach RMB 2.40 trillion in 2020.

O2o and e-commerce introduce home decoration, and concepts such as customization and decoration are gradually emerging.

A large number of stadiums and exhibition venues have been built and reconstructed.

With the rapid development of China’s real estate industry, home decoration has become a hot segment of the building decoration industry in recent years.

More types of leading enterprises are listed, and the industry concentration has increased.

Among them, the office space is mainly office buildings, the commercial area is mainly commercial centers, hotels, business places, etc., and the infrastructure buildings mainly include health places, educational places, cultural places, national institutions, etc.

This is mainly because China has hosted large-scale international events such as the Beijing Olympic Games and the Shanghai WorldExpo.

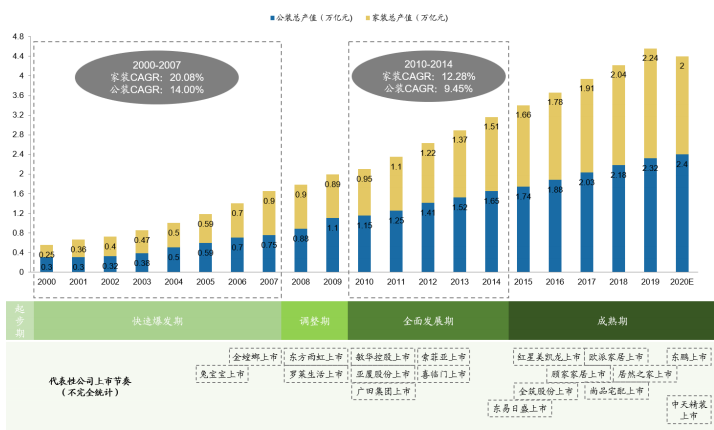

From the time dimension, China’s architectural decoration industry can be roughly divided into five periods: (1) initial period.

In 2017, the National Bureau of statistics officially revised the classification of the building decoration industry.

The decoration industry is the product of China’s economic system reform and opening-up, and it is also the first industry in China to introduce market mechanism and carry out market-oriented operation.

Table 1: classification data source of decoration industry: National Bureau of statistics, China Architectural Decoration Association and GF Securities Development Research Center.

Figure 1: data source of the development stage of China’s building decoration industry: EU think tank, Deloitte decoration, GF Securities development research center according to the data compiled by EU think tank, the total output value of China’s decoration industry increased from 1.99 trillion yuan to 4.56 trillion yuan from 2009 to 2019, with an annual compound growth rate of 8.65%; Among them, the total output value of home decoration increased from 0.89 trillion yuan to 2.24 trillion yuan, and the total output value of public decoration increased from 1.10 trillion yuan to 2.32 trillion yuan.

(2) Rapid outbreak period.

Yasha shares, Guangtian group and other enterprises were listed during this period, which continuously brought new impetus to the development of China’s architectural decoration industry.

Today’s Golden Mantis, the leader in the building decoration industry, and bunny, the leader in the production and marketing of the veneer industry, were successfully listed during this period.

From 2007 to 2009, the compound growth rate of China’s total output value of home decoration was 0%.

At the same time, it has driven the mass construction and transformation of hotels, airports, theatres and other facilities, resulting in a rapid growth in the public dress market.

In the loose macro environment, China’s home decoration market has ushered in a strong recovery stage.

Since the “4trillion” plan in 2008, the growth rate of gross output value reached 25% in 2009, at a historical high.

(2) After 2010, the growth rate of the gross output value of the public housing market gradually slowed down, but the market volume is still in the rising stage; In 2019, the total output value of the industry reached RMB 232million, with a year-on-year growth rate of 6.42%.

At this time, the real estate market tightened, the compound annual growth rate of the home decoration industry was less than 10%, and the compound annual growth rate of the public decoration industry also remained at about 7.4%.

Figure 2: data source of total output value of China’s decoration industry: EU think tank, Deloitte decoration, GF Securities Development Research Center Figure 3: data source of total output value of China’s decoration industry segment market: EU think tank, Deloitte decoration, GF Securities Development Research Center 2 market overview the growth of the public decoration market slowed down, the growth of the home decoration market increased, the acceleration of the soft decoration market was obvious, and the growth of the public decoration market slowed down gradually, The industry scale tends to be stable, and the public building decoration covers a wide range, including office space, commercial area and infrastructure.

During the development process, the market scale shows an upward trend, and the industry has entered a mature stage.

After 2015, China’s decoration industry has entered a mature period.

Concepts such as precast decoration and Internet home decoration are constantly emerging.

In 1997, China officially promulgated the construction law of the people’s Republic of China, and the building decoration industry began to start.

The industry is in a period of rapid explosion.

During this period, leading building materials enterprises with high degree of standardization and resource barriers gradually formed, and Dongfang Yuhong and Luolai life were listed during this period.

(4) Comprehensive development period.

The global financial crisis in 2008 has greatly affected China’s home decoration industry.

From 2010 to 2014, the growth rate of China’s public decoration industry gradually slowed down, and the compound growth rate of the total output value fell back to 9.45%, while the compound growth rate of the total output value of the home decoration industry rebounded to 10%.

(3) Adjustment period.

(5) Maturity.

After the abolition of welfare housing and the monetization of housing in 1998, the decoration industry in the form of a company gradually took shape.

According to the data of EU billion think tank, the total size of the home decoration market in 2020 was about 3.54 trillion yuan, with a compound growth rate of more than 11% in five years..

In 2007, before the outbreak of the financial crisis, the total output value of China’s building decoration industry was 1.65 trillion yuan, including 0.9 trillion yuan for home decoration and 0.75 trillion yuan for public decoration.

According to the data of yiou think tank and Deloitte decoration: (1) from 2002 to 2009, the public dress industry was in the stage of accelerated expansion.

Due to the expansion of national infrastructure investment, the growth rate of the total output value of the public decoration industry reached more than 20% during this period.

From 2000 to 2007, the compound growth rate of household decoration output value continued to be higher than 20%, and the compound growth rate of public decoration output value reached about 14%.